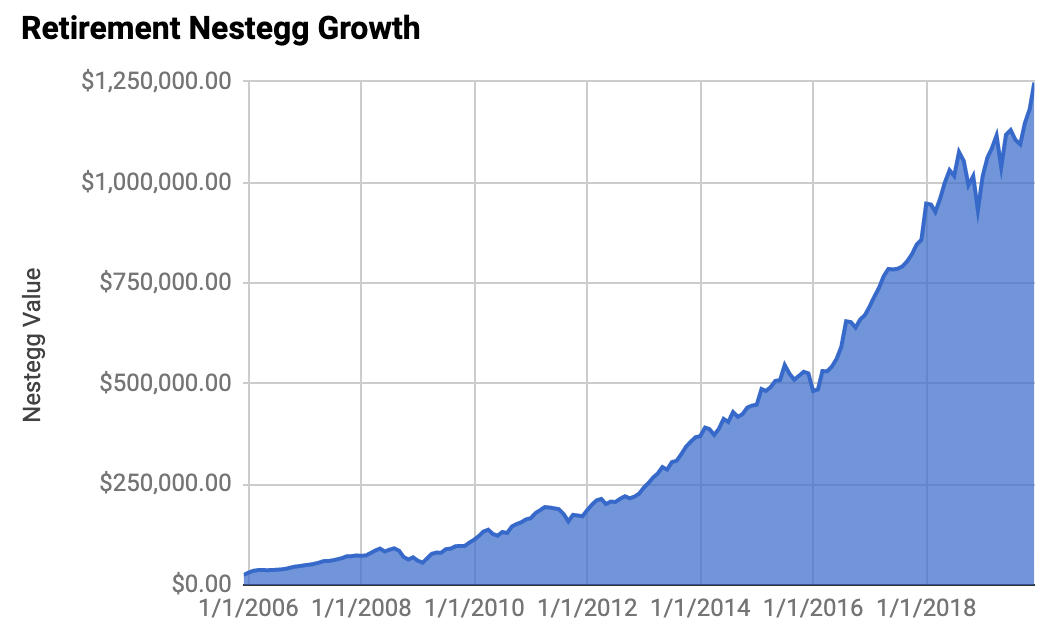

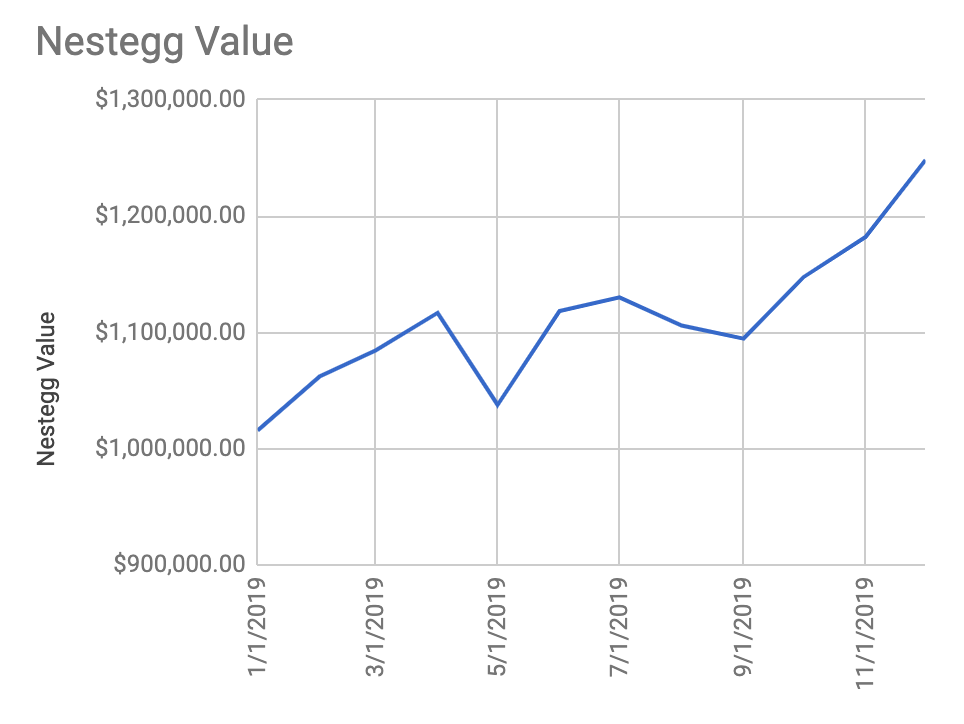

Well the conclusion to a stellar year for my retirement nestegg. It increased in value by over $317,500 in 2019, which is absolutely mind boggling. Granted it was a great year for the market overall and somewhat of an anomaly, but the fact that I had to do zero work or use any brain power and we got $300,000 richer in a year is sort of bonkers.

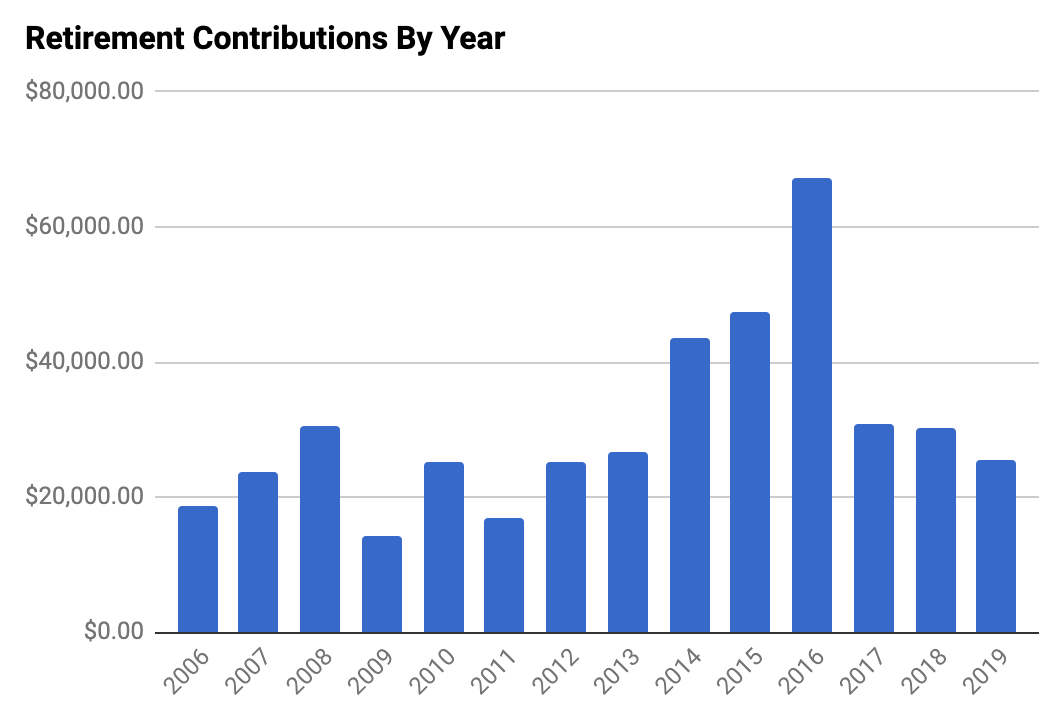

The stock market was up over 28% this year and my investments were up even more than the market for the year. My contributions on the other hand were the lowest they’ve been in about 10 years as I’ve decided to let the portfolio do the heavy lifting here (working out ok so far).

If I really want to drop my own jaw I simply only need to go back to the end of the last decade where my December 2009 Financial Report where I was sitting at a grand total of $105,415.89 and was feeling pretty good about finishing a month in 6 figures for the first time. Now 10 years later I increased my nestegg by over 3 times the value of my Dec 2009 report. That’s the magic of compounding.

So what does my Dec 2029 report have in store? Will I increase the value of my portfolio by $3.75M in a year? Who knows and honestly it doesn’t matter as accumilating the most money possible is not the goal of this blog. It’s about accumilating enough money as quickly as possible to give me and my family the freedom to not have to worry about money and for all intents and purposes we are already there so everything from here on out is simply gravy.

Taxable Account- $70,069.58(+13.23%)

Private Stock $72,000 (+0.00%)

Traditional Rollover IRA – $43,987.57(+3.91%)

My Roth IRA – $307,347.80(+8.82%)

Wife Roth IRA – $195,227.71(+7.98%)

Wife 401k – $4,756.71(+2.99%)

Traditional 401k – $554,871.58(+3.15%)

Roth/Traditional % = 40.26% (tax free)

Total Retirement Nest Egg $1,248,260.95(+5.61%)

Retirement Salary (4%) $49,930

Monthly Contributions $1,354.98(401k)

SP500 Performance +2.86%

My Monthly Investment Performance +2.94% (-0.47% vs SP500)

My Monthly Individual Stocks Performance +3.10% (-0.31% vs SP500)

My retirement contributions for 2019 $25,366.43

401k $13,117.48

401k matching $12,248.95

My Roth IRA $0

Wife Roth IRA $0

Taxable Account $0

Wife Retirement Account ??

SP500 Performance for 2019 28.72%

Investment Performance for 2019 +32.46% (+3.74% vs SP500)

Individual Stock Performance for 2019 +37.07% (+8.35% vs SP500)

Total Investment Return 2019 +$292,164.67