Oof. Wow what a year. I don’t even know how to put into words how crazy this year was. Obviously everything going on with a global pandemic and all of the horrible things that everyone has had to deal with this year has been at the forefront of everything 2020. One would logically think that 2020 would have been a horrible year to be an investor and once the pandemic hit I would have agreed 100% with that statement and I’m not sure many experts would have disagreed either.

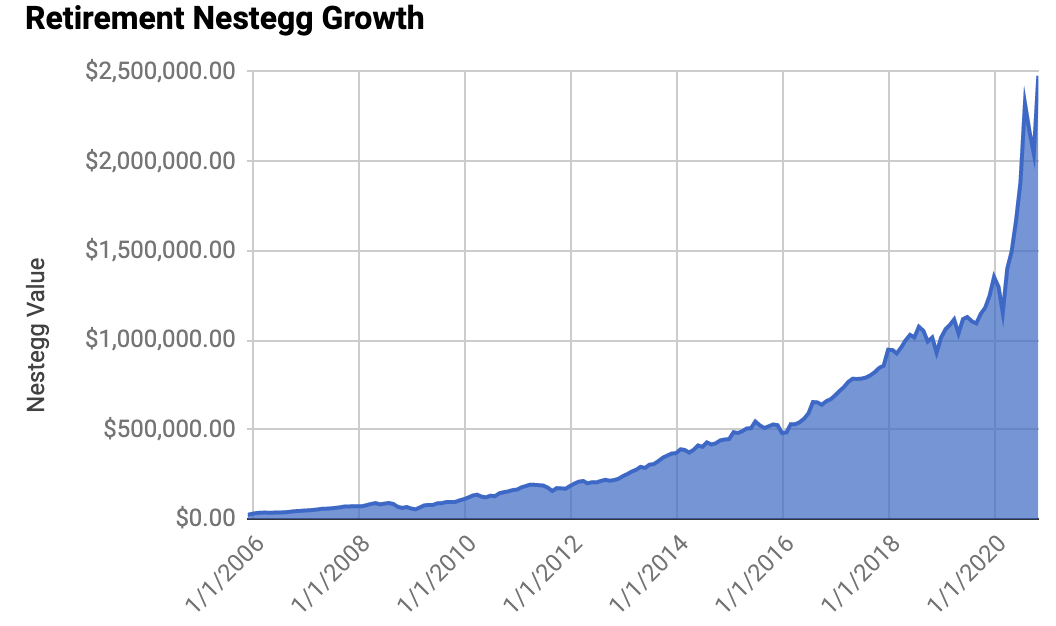

Fortunately this is now not my first rodeo and I have experience of the benefit of doing absolutely nothing and this year it paid off in spades. My retirement nestegg over doubled ending the year up 117%. This was driven in a very large part by my individual stock portfolios which ended the year up 218%, which was driven in large part by the meteoric stock rise of Tesla which was by far my largest holding.

Our investment gains for 2020 were just short of $1.5 million. To put that in perspective all of my investment gains for the prior 14 years were only $890k and well my entire nestegg was only worth $1.2M going into this year. That’s the power of compounding in full force and well obviously our returns supercharged everything.

I will be the first to admit that I am extremely lucky. I have hit some massive homeruns with some of the best individual stock performers in the last 20 years (Netflix, Amazon, Tesla). My Tesla position now makes up $1M of my portfolio and that amount very well could be $0 as Tesla could have gone bankrupt. I definitely took some small educated risks over my career and some of them have paid off handsomely.

The thing is I didn’t need to be lucky. I didn’t need to take risks. Simply living below my means and putting my money in index funds has resulted in me having a sizeable nestegg that gives me tons of future freedom. I have contributed significantly more to my index funds and I started very early in this journey. This gave me the freedom to take some risks without really risking anything at all. If everything blew up in my face with my individual stock portfolio I was still going to be very ok and still on track for an early retirement. I already had my pile of F-you money. This gave me the freedom to take risks with parts of my portfolio and with my career choices.

F-you money money opens up so many new doors for you and I highly suggest you start accumilating your own pile of F-you money.

This now marks 15 straight years that I have published my retirement nestegg report. In that time it has grown from $24,616 to today’s total of $2,761.505. This has been incredibly valuable to me as I tracked my progress against my financial goals. Going forward this number really doesn’t mean much to me anymore and I really don’t have much more to accomplish. In that respect I’ve made the decision to stop publishing my monthly reports going forward.

I proved my point that by simply living frugally and investing for the long term over a period of 1 or 2 decades will result in more money than you could ever need. It wasn’t complicated. You didn’t need to win the lottery. You didn’t need to be a professional athlete. Just spend less than you earn, invest it, and let time work its magic.

Fidelity Taxable – $6,025.88(+10.24%)

Taxable Account- $331,736.27(+20.49%)

Private Stock $82,500(+0.00%)

Traditional Rollover IRA – $116,164.46(+16.30%)

My Roth IRA – $1,010,837.95(+15.35%)

Wife Roth IRA – $531,398.11(+9.38%)

Wife 401k – $5,577.30(+2.69%)

Traditional 401k – $677,265.58(+4.69%)

Roth/(Traditional+Taxable) % = 55.85% (tax free)

Total Retirement Nest Egg $2,761,505.55(+11.45%)

Retirement Salary (4%) $110,460

Monthly Contributions $933.84(401k)

SP500 Performance +3.71%

My Monthly Investment Performance +11.42% (+7.71% vs SP500)

My Monthly Individual Stocks Performance +14.55% (+10.84% vs SP500)

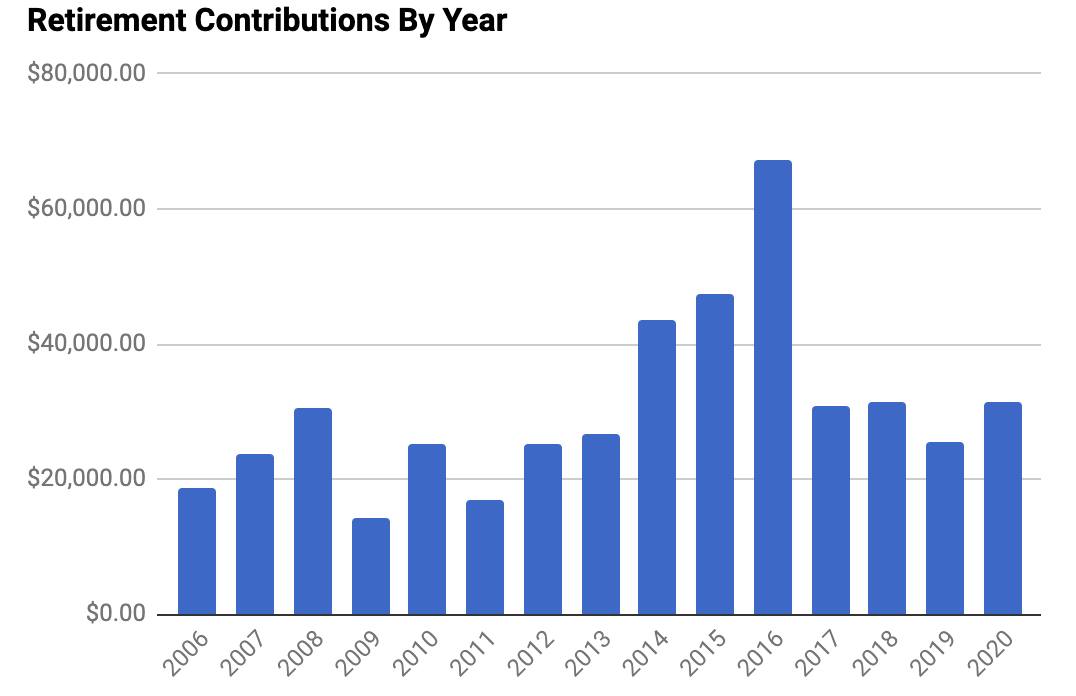

My retirement contributions for 2020 $31,376.37

401k $7,174.31

401k matching $12,302.06

My Roth IRA $0

Wife Roth IRA $0

Taxable Account $$11,900.00

Wife Retirement Account ??

SP500 Performance for 2020 +16.26%

Investment Performance for 2020 +117.02% (+100.76% vs SP500)

Individual Stock Performance for 2020 +218.49% (+202.23% vs SP500)

Total Investment Return 2020 +$1,481,868.23