I lost $1 million dollars

Well this is another goal of mine which sounds counterintuitive, but in my October 2018 Retirement Nestegg Report I was commenting about how losing $100k in a month was a non event for me and then made this statement

My goal some day is to lose $1 million dollars in portfolio value.

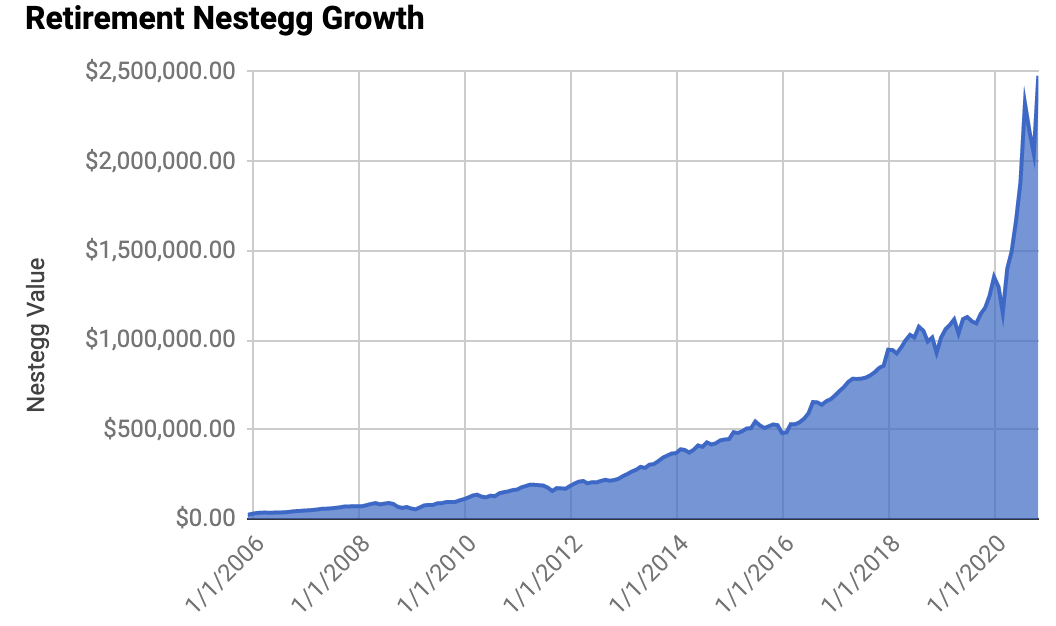

Well today after a few weeks of carnage it occurred to me that I may have lost about $1 million dollars on paper and sure enough my portfolio set an all-time high on Nov 4th of 2021 and now today just 79 days later my portfolio has fallen more than $1 million dollars below that ATH. Mission Accomplished!!

A couple of thoughts on this.

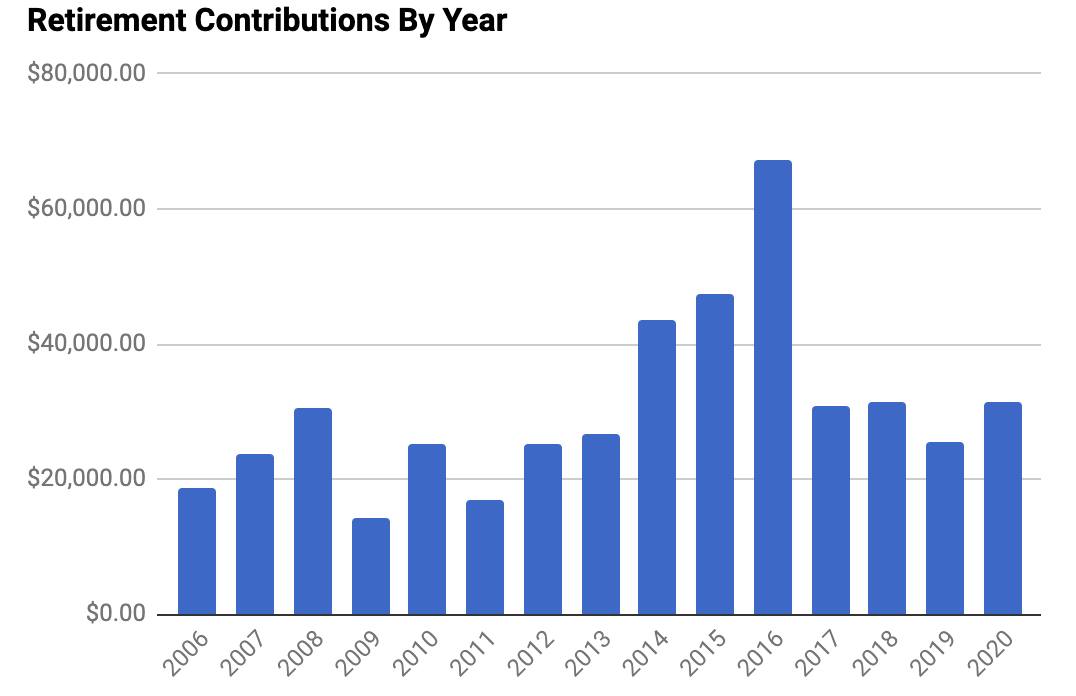

I originally made that statement because in order to lose a million dollars you have to have a fairly large sum of money – hopefully quite a bit more than $1 million, but at least $1 million. So if someday I lost $1 million dollars that probably meant that I was doing pretty good and was in pretty good shape and the $1 million dollars was not going to be as devastating as it sounds. Percentages of big numbers are big numbers. They can work for you and against you and while I lost $1M in 79 days I gained more than $1M 64 days to hit that all-time high.

I also lost $1M and to be honest it really has added zero stress to my life. Like I mentioned I lost $1M and am back to the same portfolio I had in September. Easy come, easy go. Volatility and fluctuations in the market are normal and the price you pay for the performance. I never in my wildest dreams expected to be hitting the numbers that I have hit the last few years and so taking things down a few notches really doesn’t make me feel like I’m somehow behind schedule, in fact I’m still currently wildly ahead of schedule and have a sum of money that has me in great shape for the rest of my life.

Nothing has changed. I still own all of the same businesses I did 79 days ago and their business prospects have not materially changed. All of the factors outside of their control and my control have changed. Investor sentiment is a very fickle thing that swings wildly out of control in either direction, but at the end of the day it affects absolutely nothing other than the short term prices. Case in point for much of Tesla’s existence and them building up their company to one of the best business models in the world, investor sentiment was very much against their company and their CEO. None of that however affected what the underlying company was doing and the profits that they would be making in the future. Same with my portfolio. I feel very good about the prospects of my individual companies I own and the health of the largest companies that drive my index fund performance and over a 5 or 10 year period I will not even be able to pick out this spot on the chart of where I lost $1M. Just like the great recession does not show up on a long term chart of my nestegg growth.

Also while I am starting to tap into some of my nestegg for early retirement, do not need the vast majority of these funds for many years so the fact that my portfolio is up or down and hit a certain number today doesn’t mean anything to my future prospects unless I let it dictate my emotions and do something stupid and change my course. Just like no single day, month, or year made one iota of difference of where my portfolio is today. This is a long term game and while it’s nice to check in on progress from time to time you need to stay focused on the big picture and just keep doing the same small daily habits that have huge effects on your long term future.

I feel like I’ve made some crazy predictions on this blog and every single one of them have come true much faster than I ever could have imagined. I probably should make some grand prediction about how I can’t wait to have $10M or $100M dollars some day, but to be honest that would not change my life in any meaningful way. It’s funny how important financial metrics/numbers were to me or how important I thought they were, but as I’ve now hit that area of Financial Independence I realize that things like your time and doing things you enjoy with people you love is the only thing that matters. The numbers and metrics give you that freedom and once you have that freedom the additional dollars do not affect your life in any meaningful way. The sooner you can get to that number the greater the compounding affect it has on your life, but once you are there money becomes such a minor part of the equation.

If you are still on your journey to FI, use these short term dips as opportunities. I have no idea when the market will bottom out and neither does anyone else, I very well could be writing about losing $2M, but in the meantime I will continue to enjoy the things in life that matter.